Key Market Trends Driving Product Adoption

Key Market Trends Driving Product Adoption

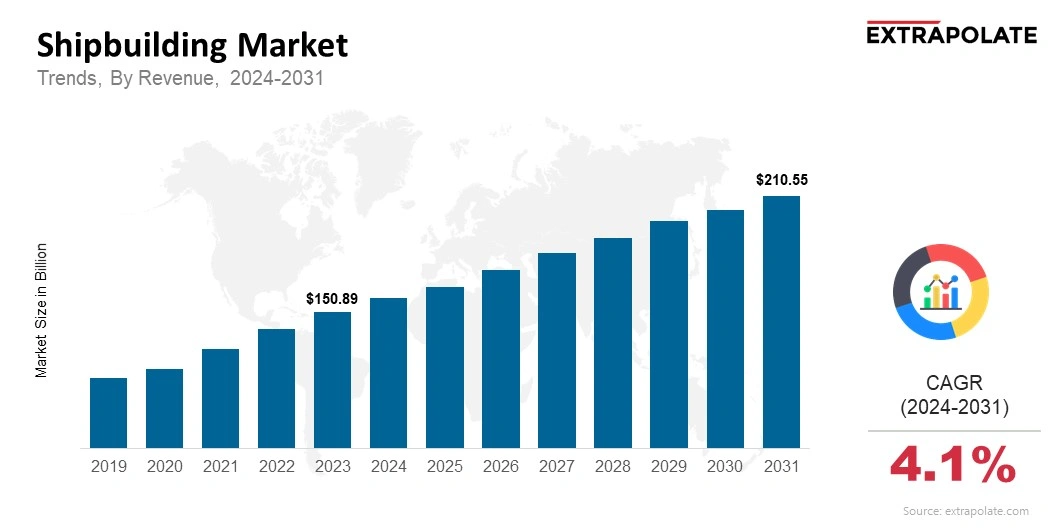

The global market is projected to reach USD 210.55 billion by 2031, growing at a CAGR of 4.1% from 2024 to 2031.

The global market was valued at USD 158.46 billion in 2024.

Key players in the market are Hyundai Heavy Industries, Daewoo Shipbuilding & Marine Engineering, Samsung Heavy Industries, China State Shipbuilding Corporation, Mitsubishi Heavy Industries, Fincantieri, STX Offshore & Shipbuilding, Damen Shipyards Group, Japan Marine United Corporation

Key factors that are driving the Shipbuilding Market Advances in Upgrading naval fleets and investing in military ships helps the defense shipbuilding industry. Countries are investing in infrastructure to boost the cruise and ferry industries.