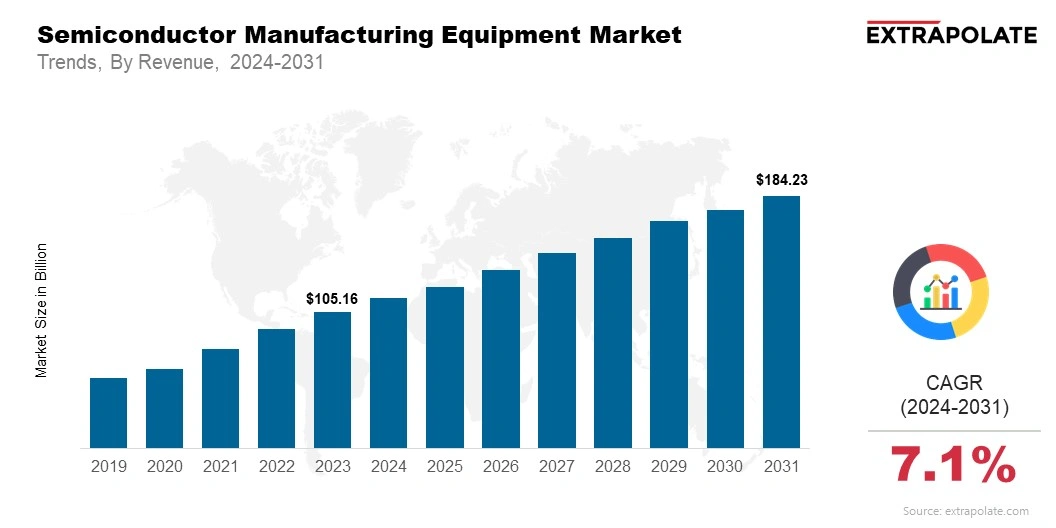

The global market is projected to reach USD 184.23 billion by 2031, growing at a CAGR of 7.1% from 2024 to 2031.

The global market was valued at USD 113.63 billion in 2024.

Industry Demand Next-generation technologies rise. 5G, AI, and autonomous vehicles fuel semiconductor demand. Equipment manufacturers find new opportunities in this surge.

Key players in the market are ASML, Applied Materials, Lam Research, Tokyo Electron, KLA Corporation, ASMI, Teradyne