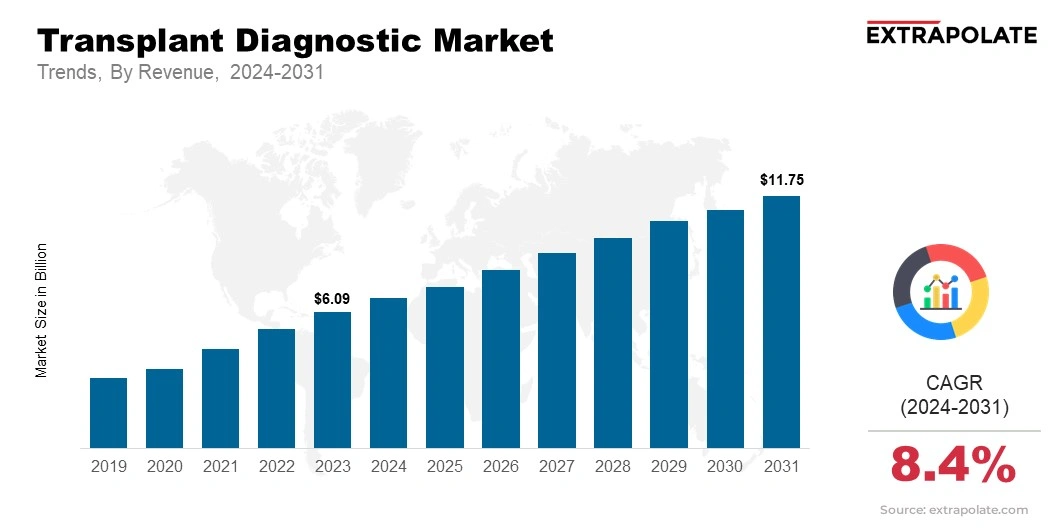

The global market is projected to reach USD 11.75 billion by 2031, growing at a CAGR of 8.4% from 2024 to 2031.

The global market was valued at USD 6.66 billion in 2024.

Chronic conditions like diabetes, heart disease, and kidney failure are increasing. This raises the need for organ transplants and diagnostic tests.

Key players in the market are Thermo Fisher Scientific, Abbott Laboratories, Qiagen N.V., Hologic, Inc., Bio-Rad Laboratories, CareDx, Inc., GenDx, One Lambda (Thermo Fisher), STRATA Pathology Services, Inc., Roche Diagnostics, and Others.