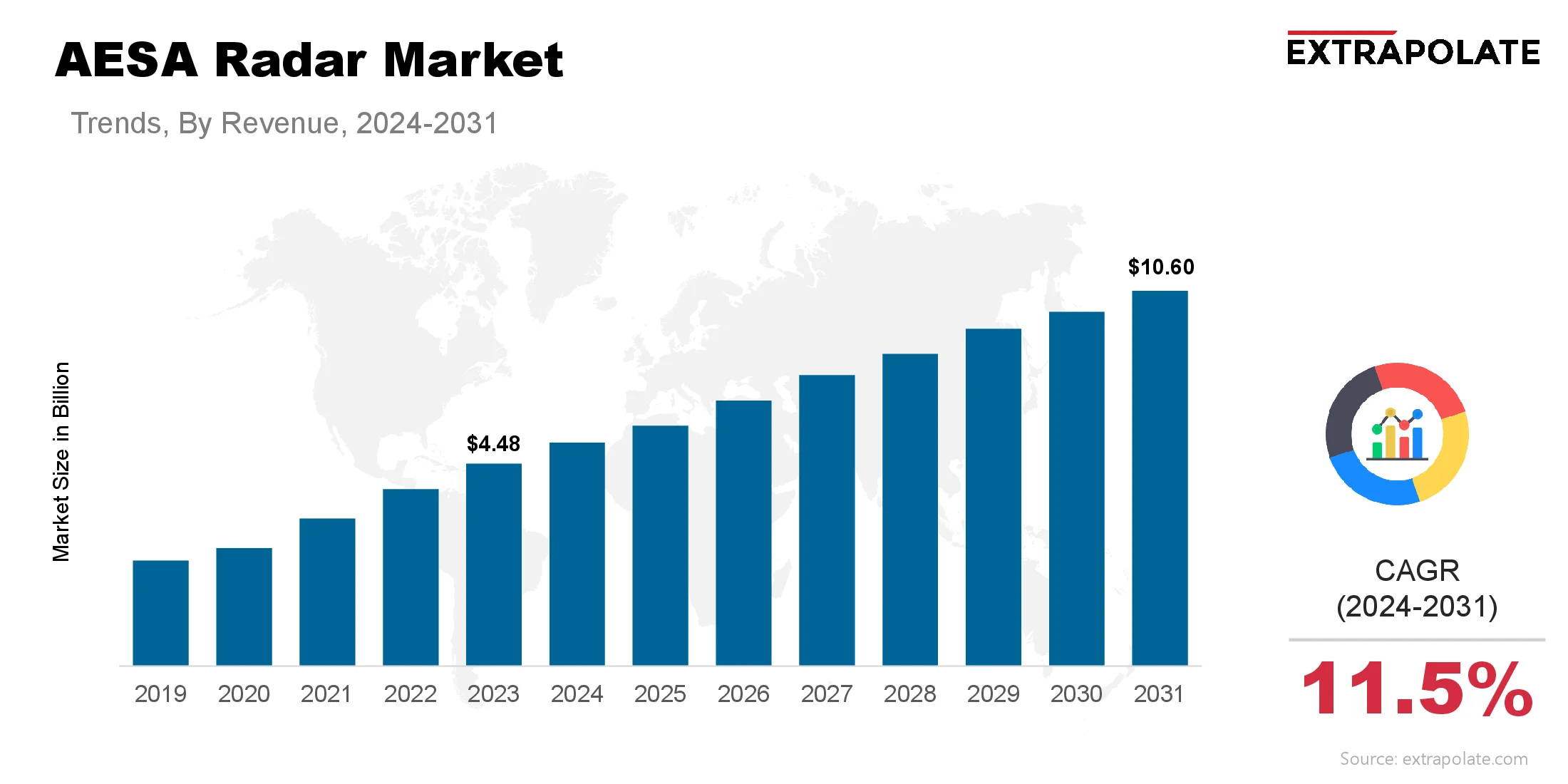

The global market is projected to reach USD 10.60 billion by 2031, growing at a CAGR of 11.5 % from 2024 to 2031.

The global market was valued at USD 4.94 billion in 2024

Nations worldwide are modernizing their defense, replacing old radar systems with AESA technology.

Key players in the market are Northrop Grumman Corporation, Raytheon Technologies Corporation, Lockheed Martin Corporation, Leonardo S.p.A., Thales Group, BAE Systems plc, Israel Aerospace Industries Ltd., Saab AB, HENSOLDT AG, Elbit Systems Ltd. and Others.

Key players in the market are Northrop Grumman Corporation, Raytheon Technologies Corporation, Lockheed Martin Corporation, Leonardo S.p.A., Thales Group, BAE Systems plc, Israel Aerospace Industries Ltd., Saab AB, HENSOLDT AG, Elbit Systems Ltd. and Others.