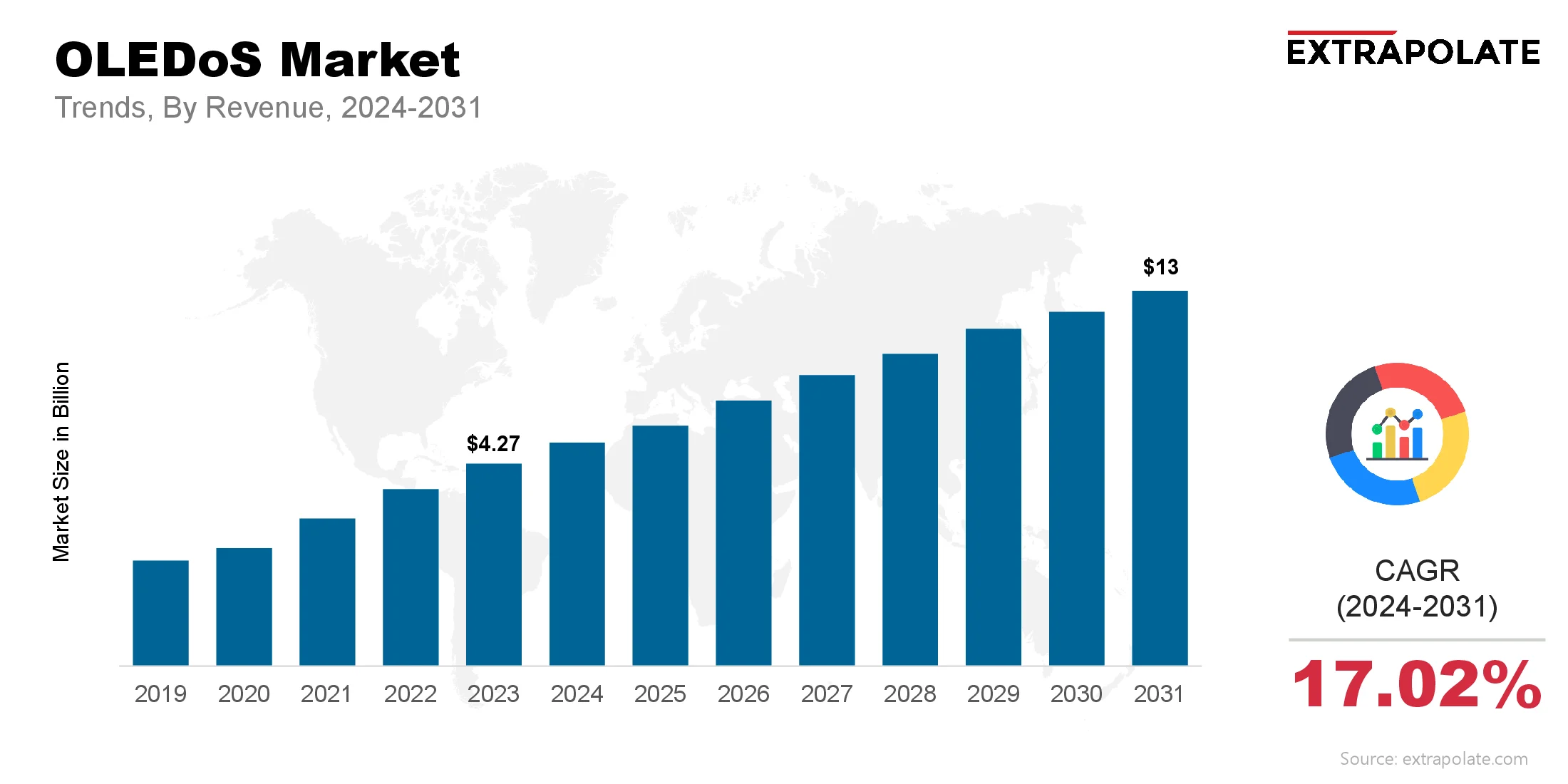

The global market is projected to reach USD 13 billion by 2031, growing at a CAGR of 17.02% from 2024 to 2031.

The global market was valued at USD 4.32 billion in 2024.

The proliferation of AR/VR devices across entertainment, enterprise training, education and healthcare has increased the interest in micro-OLED displays.

Key players in the market are Sony Corporation,eMagin Corporation, Kopin Corporation, BOE Technology Group, Seeya Technology,Olightek, Jade Bird Display (JBD), Panasonic Holdings Corporation, INT Tech,AU Optronics and Others.